Insurance product design today must satisfy two forces at the same time: market demand and regulatory control. Every product decision (coverage logic, pricing assumptions, user flows, and updates) must stand up to board oversight, compliance reviews, and regulatory frameworks. For example, EIOPA POG, FCA Consumer Duty, and state-level filings.

Clear product architecture, transparent decision rules, and structured governance make products easier to approve, operate, and evolve. In this article, our Arounda team explains how we design products that remain compliant, understandable, and manageable throughout their lifecycle.

Article Key Takeaways

Our experts explain how insurance product design and development should align with regulatory requirements and board oversight.

You’ll get:

- Expert insights into how regulatory frameworks shape insurance product design and development

- Common pitfalls in insurance product design and how to avoid them

- Practical strategies for keeping products adaptable within legal boundaries

- Best practices for creating robust product architecture that ensures long-term stability

- Approaches for aligning product design with board governance and compliance requirements

- A closer look at product approval committees and how they affect design decisions

From Product Launch to Product Governance

Insurance products move into governance the moment they enter real operations. After launch, product structure starts affecting compliance, internal control, approvals, and everyday product decisions across the business.

The Shifting Design Mandate

Creating an insurance product starts with decisions that will hold up after launch. The product needs to stay clear in use, consistent across teams, and controllable inside a regulated environment.

We asked our COO, Alexey Kovalchuk, to reflect on what this means in practice for insurance product work.

“When our design teams create insurance products, we can’t stop at screens, flows, or launch preparation. We also have to think through product conditions, decision rules, internal handoffs, and review points. And make it practical. Design starts influencing product logic and operational structure early on, because those decisions affect how clearly the product will be understood, approved, and managed later.

Alexey Kovalchuk, COO at Arounda

The Hidden Cost of Poor Product Architecture

Poor product architecture creates problems that become visible only after launch, when the product starts moving through real workflows, approvals, and day-to-day decisions.

Most commonly, we notice:

- Users disengage fast: Broadridge found that 59% of consumers have lost trust in a company because of a poor experience or unclear communication.

- Updates drag: if the logic is unclear, more time goes to alignment, checks, and rework.

- Operational friction spreads: underwriting, claims, compliance, and product teams start interpreting the same conditions differently.

- Governance becomes heavier: reviews and approvals take longer when product logic is harder to trace.

- Fixing it later becomes costly: once the product is live, structural changes are harder to make without disruption.

How to avoid it?

At Arounda, our designers approach insurance product software development by mapping handoffs between teams before development starts. They define where product decisions move from user flow to internal handling, so the structure stays clear across operations, reviews, and support.

What Good Insurance Product Design Actually Looks Like

Good insurance product development depends on a few core design decisions that shape how clearly the product works in practice. The most important of them usually appear in coverage coherence, product sustainability, and the quality of early product definition.

Coverage Logic and Policy Coherence

Good insurance product development starts with internal consistency. Coverage should be clear in every section, with no contradictions or confusion. The core logic must align across the offer, conditions, and user experience.

What this usually requires:

- Clear coverage boundaries

- Aligned conditions and exclusions

- Consistent claims logic

- Coherent product wording

- Shared interpretation across teams

What do we recommend?

To keep coverage logic and policy structure aligned in practice, create a rule matrix before development begins. Map each coverage condition to user actions, system behavior, and internal review points. This helps the team catch gaps early and keeps product logic consistent across the whole experience.

Sellable vs. Sustainable Products

Sellable products can attract attention quickly, but sustainable products are what strong insurance design should aim for. They stay manageable after launch, support cleaner updates, and hold their structure as product demands grow.

A sustainable insurance product usually has:

- A clearer product structure

- A manageable level of complexity

- Easier updates and adjustments

- Stronger consistency across flows and product logic

- Less reliance on manual fixes or workarounds

Where Product Teams Fail Before Actuarial Starts

Many product issues appear before actuarial work begins. Teams move too quickly from concept to build, while key parts of the product still remain unclear in use, overloaded with exceptions, or disconnected from operational reality.

Common failures include:

- Unclear product promise

- Early complexity without a clear priority

- User journeys that do not hold up in practice

- Gaps between customer-facing flows and internal handling

Arounda design and development teams help resolve these gaps before they turn into delivery and product issues. Our designers clarify the product offer, simplify the experience, and define flows that make sense for both users and the business behind the product.

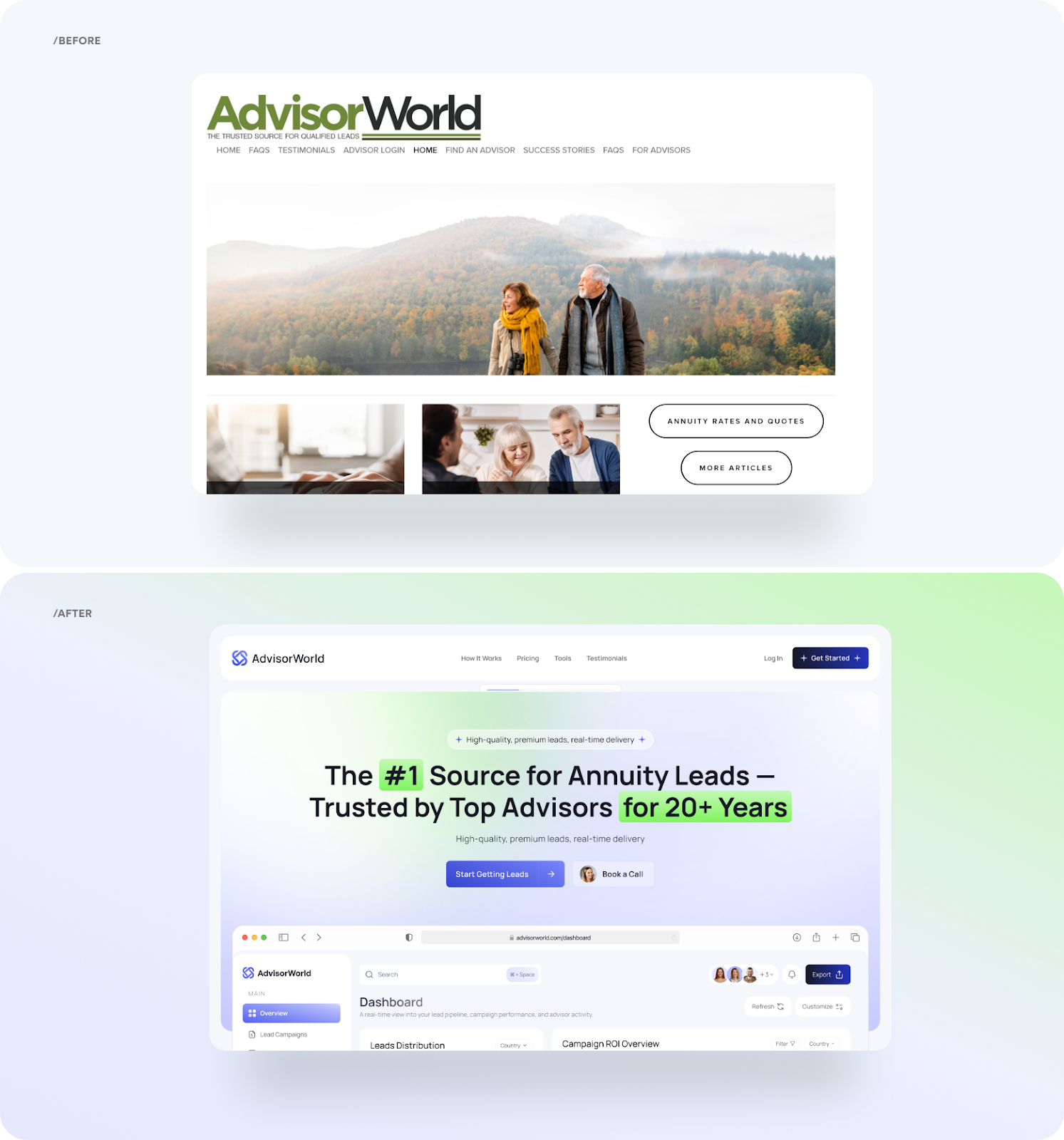

A good example in this regard is a B2B fintech platform for financial advisors, AdvisorWorld. The product needed a more coherent digital presence, clearer structure and flow, and an explanation of value that didn’t create confusion.

We rebuilt the experience around the client’s B2B goals, created a custom design system, added a guided “How it works” flow to the site, and rebuilt the platform UX with a stronger hierarchy, clearer messaging, and more confidence building UX to get them +62% higher lead conversion and 35% faster onboarding.

Regulatory Frameworks That Shape Design

The insurance product design regulatory compliance framework shapes a product long before launch, influencing decisions already at the design and build stage. That pressure comes through several different frameworks, each affecting product work in its own way, from governance and customer protection to filing discipline and audit expectations.

EIOPA POG Guidelines

EIOPA’s Product Oversight and Governance guidelines require insurers to define the target market clearly and continuously review how the product performs throughout its lifecycle. These insurance product software development regulatory requirements make a few things especially important:

- Clearer product structure

- Stronger alignment with target users

- Better consistency between product logic and distribution

- Easier product review and ongoing updates

Our recommendation: Use a lifecycle review to check whether the product still fits the audience it was designed for. Under EIOPA POG, that fit matters not only at launch, but also after updates, new channels, and product changes.

FCA Consumer Duty

The FCA’s Consumer Duty raises the bar beyond formal compliance. Its focus is on whether a product leads to good customer outcomes, which makes its clarity a much more practical design issue. For teams working on FCA consumer duty insurance product design implications, this usually means three things:

- Clearer product presentation and fewer points of confusion

- Easier understanding of value, conditions, and product decisions

- Better visibility into where journeys create friction or poor outcomes

How to get this? Review product clarity through real user decisions, not just screens and wording. Teams need to see where value becomes harder to understand and where the journey starts creating avoidable friction.

NAIC and US State-Level Filing Dynamics

The NAIC supports regulatory coordination across the US insurance market, while product approval is largely driven by state-level filing and review. This creates a practical focus on form and rate alignment, controlled product variations, and documentation that can hold up across jurisdictions. This means:

- Clearer handling of state-level product variations

- More structured product updates

- Stronger alignment between rules, flows, and disclosures

- Better control over product changes across time

Practical takeaway: Split state-specific rules from the core product logic early. That gives teams a cleaner way to update filings, disclosures, and variations without touching the whole product.

What Regulators Actually Audit

Whether it’s EIOPA POG, the FCA’s Consumer Duty, or US filing practice, the review usually comes down to a few core areas. In practical terms, regulators look at whether the product is clear, appropriately approved, understandable to its intended users, and manageable over time. Here’s a quick view of what insurance product requirements normally matter most in reviews.

Board Oversight and Product Approval Architecture

The board oversight insurance product approval process brings product, risk, compliance, and leadership into the same approval path. And how does this influence the design decisions?

Risk Appetite as a Design Constraint

Risk appetite determines the limits on features, conditions, and decision logic, ensuring the product doesn’t exceed the level of exposure the business is willing to bear. In this context, risk management in insurance product development directly defines the product’s boundaries and the level of control required from the outset.

This influences:

- The level of complexity a product can carry

- How teams define coverage limits, exclusions, and conditions

- The points that require stricter rules in flows, approvals, or edge cases

- How teams design product features to keep them practical, controlled, and sustainable

Our tip: Add risk checkpoints directly into the flow. For example, place validation steps where eligibility, coverage limits, or policy conditions might create exposure. This allows the product to remain flexible, but keep risk decisions visible and controlled.

Product Approval Committees

Product approval committees turn risk boundaries and business priorities into real product decisions. That is why insurance product approval committee structure best practices are mostly about giving teams a clearer approval process and fewer unexpected issues late in delivery.

In practice, a stronger committee structure usually includes:

- The right mix of roles: product, underwriting, actuarial, risk, compliance/legal, operations, and technology

- Clear ownership and decision rights: who proposes, who challenges, who approves

- Early review points: the committee reviews key decisions before the product is “locked”

- A shared view of the product: one consistent set of logic, assumptions, and trade-offs

From Arounda’s experience, product approval committees add the most value when they clarify open questions before they reach design and development. Once uncertainty moves into the product itself, teams start compensating with extra logic, exceptions, and workarounds.

Three Lines of Defence in Product Lifecycle

The three lines of defence model clarifies how different functions take responsibility for a product throughout approval, launch, and ongoing use.

- 1st line (Product / Business): the teams closest to the product own day-to-day decisions and how the product works in practice

- 2nd line (Risk / Compliance): these functions review those decisions, set control boundaries, and challenge areas that may create risk

- 3rd line (Internal Audit): this line provides an independent view on whether the wider control and governance process is actually working

For design and development, this matters because product decisions stay visible long after launch. If the product logic is clear and changes are easier to trace, the product is much easier to review, question, and update without creating unnecessary friction later.

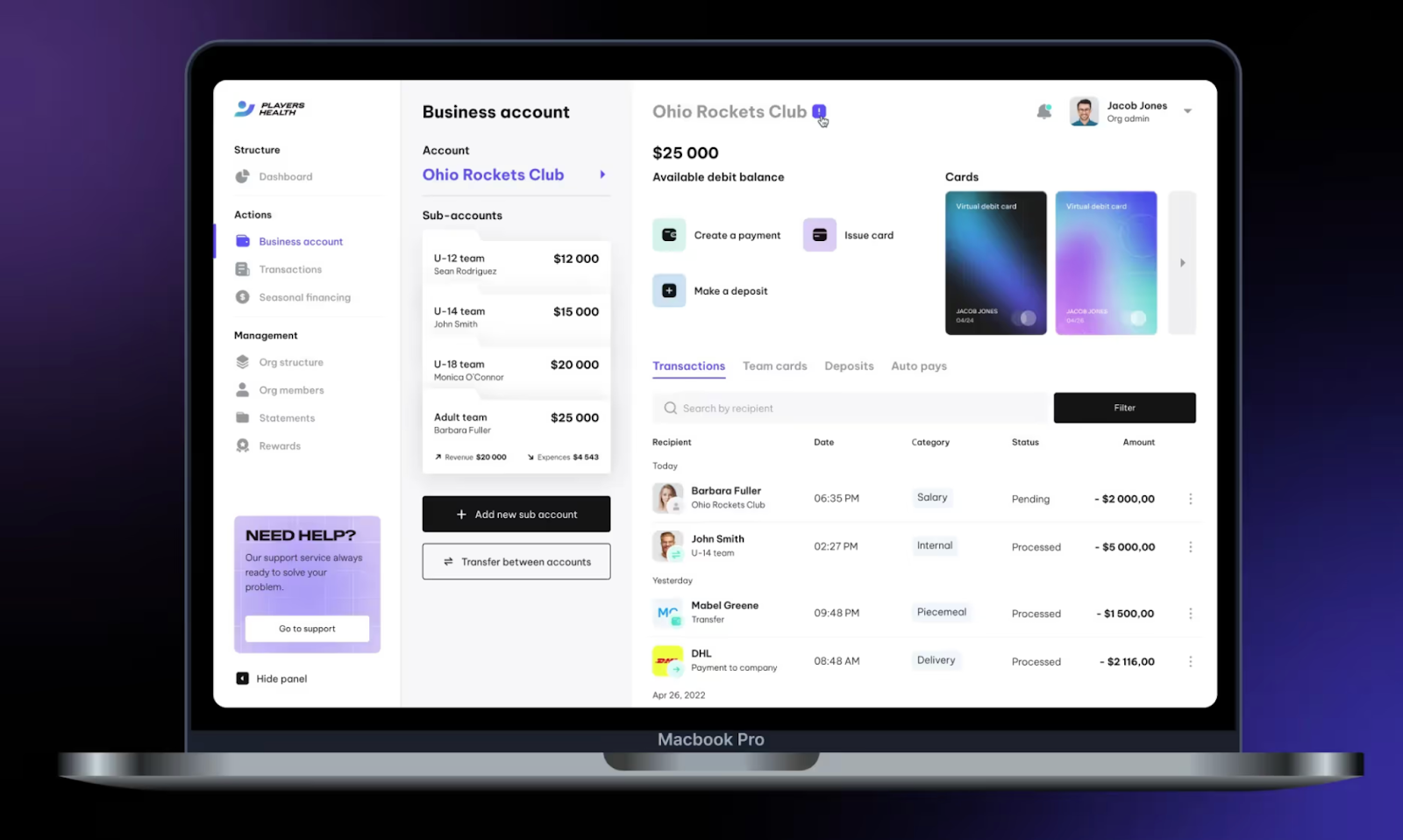

That was the context of our work with Player’s Health, a finance and insurance platform for youth sports organizations. The challenge was to simplify onboarding, structure a clear user hierarchy, and design a cleaner policy purchase flow inside a multi-account system. Our team broke registration into guided steps, improved the hierarchy between parent and sub-accounts, and reduced policy purchase to a few clear actions.

As a result, Player’s Health reduced operational costs by 33% and improved customer satisfaction by 25%.

Actuarial and Risk Architecture

The insurance product development risk management architecture behind pricing, claims, and coverage decisions plays a central role in the product structure from the start. This is where product design and development begin to intersect more closely with the assumptions that determine how it performs under real conditions.

Pricing Assumptions as a Design Variable

Pricing assumptions determine whether an insurance product is financially viable. They are based on expected claims, operational costs, and the level of risk the company is willing to accept. Because of this, pricing often defines the product itself.

In practice, actuarial analysis frequently leads teams to adjust coverage limits, product features, or policy conditions early in development. This is why pricing becomes part of product design rather than something handled later as an operational step.

Claims Scenario Modelling

A strong insurance product should work not only at the point of sale, but also when a real claim occurs. Claims scenario modeling helps you test whether your product still makes sense once users move beyond the ideal journey and rely on the actual coverage terms.

We uncover major problems during UI/UX audit. In one of our recent cases, we saw unclear coverage boundaries, weak product logic, and gaps between the product promise and the real claims experience.

What do we recommend?

Take one claim scenario and trace it through the whole product before launch. If the offer, policy wording, and claim outcome do not lead to the same decision, the product needs revision.

Stress-Testing Coverage Logic

The objective of stress-testing is to assess whether your product is valid in an impractical manner, in addition to testing its validity in clean, solid conditions. The focus during this part of the stress-testing phase is on situations that demonstrate weak structure:

- Unclear scenarios

- Overlapping conditions

- Edge cases: situations that do not meet the standard definition of where the policy applies

What do we recommend?

A practical way to use stress-testing is to isolate every case where one scenario can trigger two different outcomes. When that happens, the product needs a clearer rule hierarchy, tighter boundaries, or a narrower coverage definition.

Innovation Velocity vs. Regulatory Control

A Deloitte study found insurers are speeding up digitalization as they adapt operating models, respond to rising customer expectations, and manage cost pressure. That creates more room for insurance product innovation, but it also makes product change harder to govern, because each update still travels through systems of review, control, and approval.

However, weak product structure, unclear ownership, and approval processes that aren't designed for faster changes slow the process.

The solution: a product architecture that enables easier, controlled updates through clearer logic, defined boundaries, and better coordination between design, development, and governance.

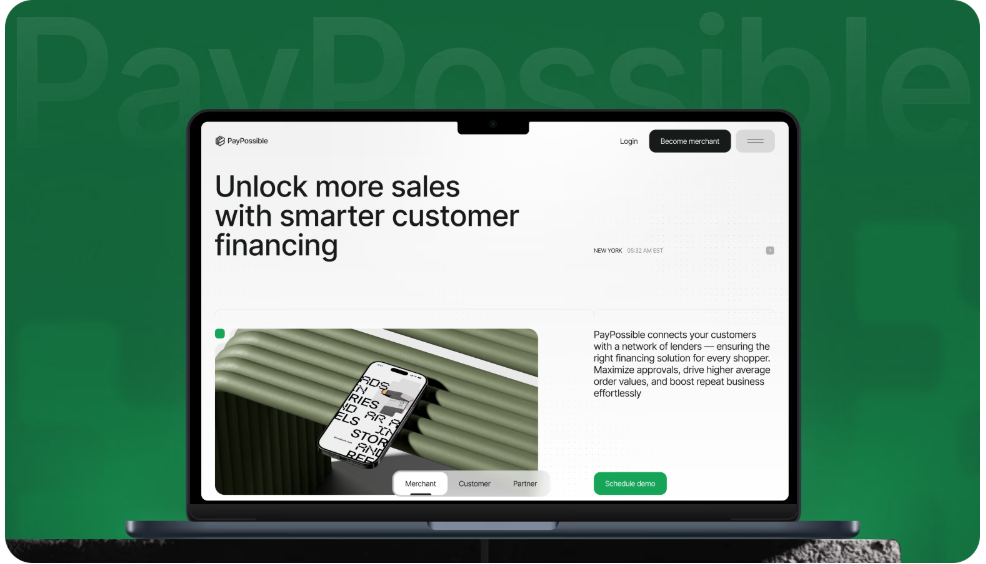

One example from our work for effective changes and modernization is PayPossible, where we redesigned an outdated website and turned it into a more structured and easier-to-use product experience.

We simplified the navigation, made the financing journey easier to follow, and presented the platform’s value more clearly for merchants, lenders, and banking partners. The result was 2x merchant signups and +40% completed financing applications.

Board-Ready Product Reporting

Product reporting becomes far more valuable when it provides visibility into not only what the product is doing but also how well it is standing up over time. A board-ready view of product performance should allow for identifying product health, emerging risk, and areas of concern to address before they deteriorate.

KPIs That Reflect Product Health

The clearest view of product health comes from a handful of KPIs that summarize usage, retention, and responsiveness to the product.

Pay attention to:

- Active users and product usage frequency

- Conversion across key journeys

- Feature adoption

- Retention and churn

- Customer satisfaction, namely CSAT or NPS

Early Warning Signals for the Board

In addition to core KPIs, leadership also needs early signals that indicate when product risk or friction is beginning to potentially take hold.

Early warning signals:

- A spike in drop-offs at a specific step of the journey

- Repeated complaints around the same topic

- Declining CSAT or NPS over a short period

- Rising churn in a specific segment or cohort

- Unusual changes in feature usage patterns

- A growing volume of support requests tied to one flow

These signals help prevent the rise of issues before they have a chance to develop into larger operational, compliance, or end-customer impact issues.

Arounda suggests:

Connect board metrics to specific product flows, features, or user segments from the start. Track where the signal comes from, what changed, and which part of the experience caused it. That makes reporting more actionable and helps teams catch product problems earlier.

What are real examples of insurance product design failures?

Most problems start from the same points:

- The product does not fit its audience closely enough.

- Its value becomes less convincing once it reaches the market.

- The claims side exposes gaps that were not fully resolved earlier.

A few recent examples show how these patterns appear in real insurance products.

1. Weak target market and value fit

The EIOPA Consumer Trends Report 2024 found that for 12 of the 26 national authorities that responded, there were non-life products found on the market that offered consumers poor value, often due to an unjustified cost or commission. This highlights a problem of product design at the foundational level.

2. Product value becomes less clear once the product reaches distribution

In its TR24/2 review, the FCA described cases where distributors assessed fair value differently from manufacturers. That kind of mismatch usually suggests that the product’s intended value, target market, or conditions were not translated clearly enough beyond the original product team. As a result, the product may start losing consistency once it moves into real distribution.

3. Claims experience reveals gaps in product logic

In its claims-handling findings, the FCA cited weak oversight, high volumes of complaints, and poor management information across claims processes. It serves as a valuable reminder that a product can appear well-designed at launch, and yet find structural weaknesses exposed later.

Conclusion

Strong insurance products do not start with one major launch decision. Teams create them through clear structure, realistic assumptions, and steady discipline across the product lifecycle. That’s what makes it easier to govern, support, and improve without layering on more complexity.

If you want your insurance product design to support long-term growth and smoother product change, contact us. At Arounda, we design and build digital platforms that make complex products clearer, more usable, and easier to manage at scale.